What is the opportunity for cross-border business growth?

As global business continues to expand, so too does the volume of cross-border payments. There are currently $120 trillion in global B2B payments processed annually. There is a predicted $10T opportunity* in the global high value cross-border payments space according to a survey commissioned by Visa, with almost six-in-ten respondents (59%) expecting overall revenues from cross-border payments to increase in the next five years as a result of faster payments. This is also supported by the combined research of Aite Group & McKinsey & Company which predicts that revenue for cross border based on transaction & FX fees will rise to an estimated $261B by 2025. Global businesses are still looking to their banks to fulfil their cross-border requirements. However, the main channels used to make international payment are still leveraging legacy methods that can be both ‘clunky’ and expensive. On average, banks in Asia Pacific have 58 Nostro accounts, which have an annual maintenance cost of more than $1.7 million.

Therefore, it is of paramount importance that innovative players start exploring new strategies such as Visa B2B Connect via Bottomline APIs to improve efficiency and maximise on revenue potential.

What is changing & why (now)?

In the face of recent B2B cross-border payments growth, banks are left to deal with these highly complex transactions that are dependent on correspondent banking relationships, offering limited visibility into the status of payments, costs, and certainty. The traditional payments process leaves receiving banks with little predictability of when payments will arrive or the amount they will receive after currency exchange calculations and various fees are deducted. Know Your Customer (KYC) and Anti-Money laundering (AML) regulations are also adding to the demand for new approaches. Complying with regional AML rules can result in transaction delays, which fosters greater concern in an already uncertain process and a current business landscape fraught with unpredictability.

With expanding global business growth, comes increased opportunities for modernization across the cross-border landscape. Banks are in an excellent position to take advantage of dynamic changes made possible by emerging technologies, such as distributed ledger technology, artificial intelligence and cloud, which are bringing greater innovation to cross-border payments. The rise of leading-edge solutions designed to reshape B2B cross-border payments will enable savvy banks to meet the shifting demands of clients.

Executing cross-border payments using the traditional bilateral corresponding process lacks transparency because both the originating bank and the beneficiary bank remain unaware where the funds of a transaction are at any given moment. Since the transaction is routed across multiple correspondent banks, knowing when payments will arrive or what costs will be incurred is essentially impossible to determine.

It is little wonder that banks view transparency into the movement of payments as a key to improving B2B cross-border payments. New digital technology innovations are entering the marketplace to address this pressing need. In a recent survey , 82% of banks worldwide viewed gaining improved visibility as one of the most appealing features of emerging payment approaches.

What does the future look like?

The business model is under pressure, and alternatives are needed even faster, with post-pandemic stimulation for digitisation, new client expectations, acceleration of the use of APIs and rich data. Banks in APAC are adopting/migrating to ISO 20022 for all their payments infrastructures as we speak (SWIFT, BahtNet, RENTAS, CHATS, PhilPass, MEPS+, …). This adoption is a catalyst as well as an enabler for the introduction of new payments rails, complementary to the correspondent banking model, and where ISO 20022 guarantees the ‘oh so important’ 100% interoperability between different cross-border payment models and platforms. Whilst ISO 20022 standardisation will help remedy many of the current pain points through improving the transparency of the payment, offering interoperability and in-turn improving operational efficiency, it isn’t a ‘solve all’.

In fact, the future of cross-border payments lies in the co-existence of new, innovative cross-border channels with the updated correspondent banking model provided by SWIFT gpi. There are a number of complementary, strategic options to choose from, that add true flexibility according to the size, priority, frequency and geography of a cross-border transaction including, but not uniquely –Singapore Faster Payments (Central Infrastructure based), non-bank solutions (e.g. Western Union) and Multilateral Payment Platforms (e.g. Visa), that was also specifically referenced by Jerome Powell, Chair of Board of Governors, Federal Reserve System “one of the keys to moving forward will be both-improving the existing system where we can, whilst also evaluating the potential of and the best uses for emerging technologies”, and in the recent G20 Report below;

This future is NOW – You Can Optimise Your Future Proof Cross-Border Payment Services Today

Your business customers are calling for more modern cross-border payment solutions.

All elements to build your strategic cross-border payments infrastructure, are available for use today, resulting in new efficiencies and new revenue streams

1. ISO 20022 provides the standardisation needed for interoperability between traditional and new cross-border channels;

2. the abundant availability of rich data and related (artificial) intelligence allows us to route payments intelligently and to choose the right channel for each transaction, whether it is to drive new coverage in markets or currencies, or to optimise the execution in existing markets;

3. the technology to enable innovation is available for cross-border: APIs, cloud, speed, security, resilience, security & operational efficiency and innovation at scale.

4. All triggered by innovation initiatives from Fintechs, incumbents and new large players, including account-to-account/PaaS, and new multi-lateral platforms.

Part of the roadmap for many banks in APAC that are connected to BahtNet & RENTAS (2022), CHATS (2023), PhilPass (2021), MEPS+ (2022), is to transition to ISO 20022. Additionally, SWIFT have said that banks need to have tested for ISO 20022 by February 2022 or they will receive a mark against their name. ISO 20022 is a central solution that also impacts real-time and open banking - all key initiatives. That aside, the impact that the richer data will have on fraud monitoring & compliance, cash-flow management and of course data and analytics provides justification enough. Therefore, it makes sense to implement a more efficient cross border solution at the same time and start reaping the benefits as soon as possible.

The potential new revenue streams via developing a new & growing fee-based pricing structure, and to cross-sell other products in your armoury and access to coveted deposits can’t be ignored. It is a brave bank decision maker that says to its board of directors and shareholders that they don’t want to take advantage of this.

How does the visa b2b connect and bottomline partnership help you lead the way?

Visa B2B Connect’s multi-lateral platform enables global payments through a single connection. For transactions between participating banks it offers an enhanced customer experience at a reduced cost and with security and efficiency through tokenisation, governance and rich data. Optional foreign exchange and same or next day settlement in multiple currencies allow for true innovation and more choice.

Bottomline Technologies is a global provider of payments solutions. As part of the Visa – Bottomline partnership, we provide cloud-native, API-based implementation of Visa B2B Connect. It is completely integrated with your existing payments infrastructure and 100% interoperable with SWIFT flows. As such, we are uniquely placed to offer banks a seamless and elegant solution for all cross-border payment flows.

How can you maximise your cross-border payment opportunities today?

The business case for updating your cross-border strategy is clear – after all, no bank is so busy or so asset rich that they don’t need to be more cost effective and turn down the opportunity to create new revenue streams via transaction fees, FX rates and cross-sell. As for the wider payments modernization piece, 86% of financial institutions agree that it is a very or extremely strong priority.

Make sure you don’t lose out to your competition and proactively seize the opportunity to be an innovator for cross border, whilst also addressing your overall payments strategy for 2021 and beyond.

*Sources: McKinsey Global Payments Map and Visa analysis.

1. Research conducted by East & Partners Europe, June 2019; Visa B2B Connect: Voice of the Customer – Banks Markets Report

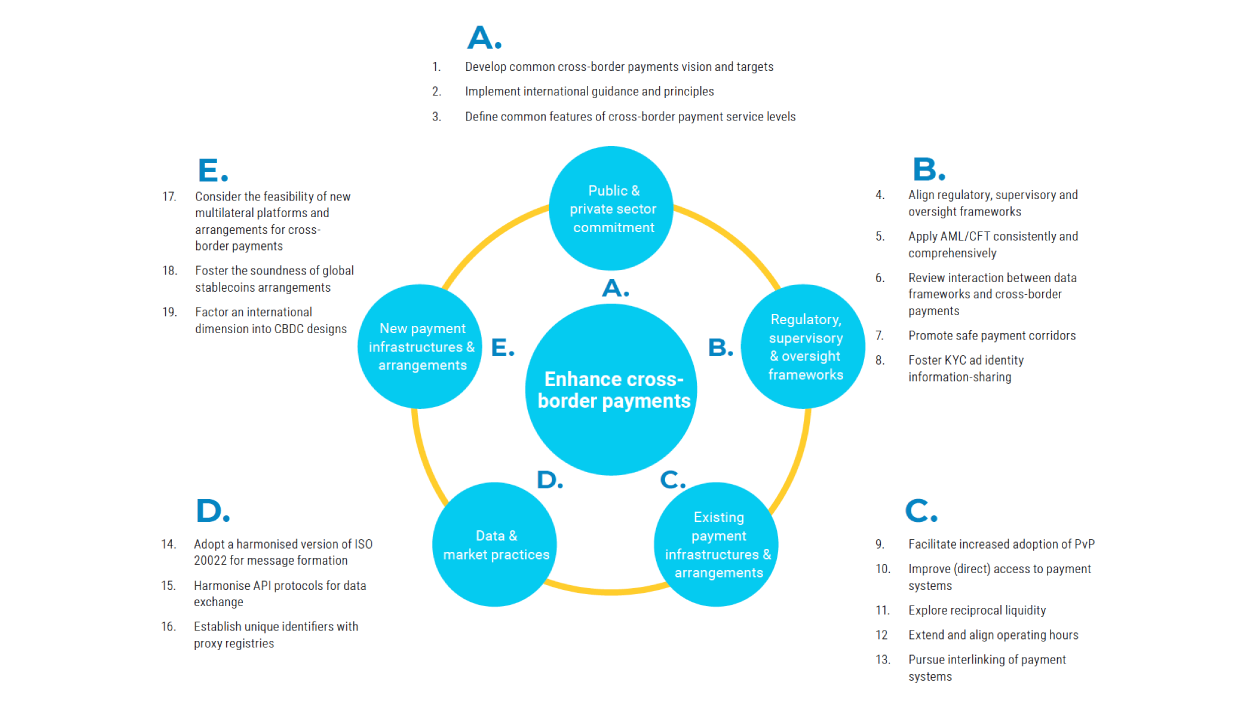

2 “Consider the feasibility of new multilateral platforms and arrangements for cross border payments”.